Let’s understand this with the example of Rajesh. He almost made a ₹2 lakh tax mistake. He’d put ₹10 lakhs into some fancy bank product that promised “market-linked returns with capital protection.” When it matured in 11 months with a nice profit, he was ready to celebrate—until his CA told him the tax bill. Because he sold one month short, his entire gain got taxed at 30% instead of 12.5%. That one month cost him ₹1.75 lakhs in extra tax. This is exactly why you need to understand listed structured investment products and their magical 12-month rule.

What Are These “Structured Products” Anyway?

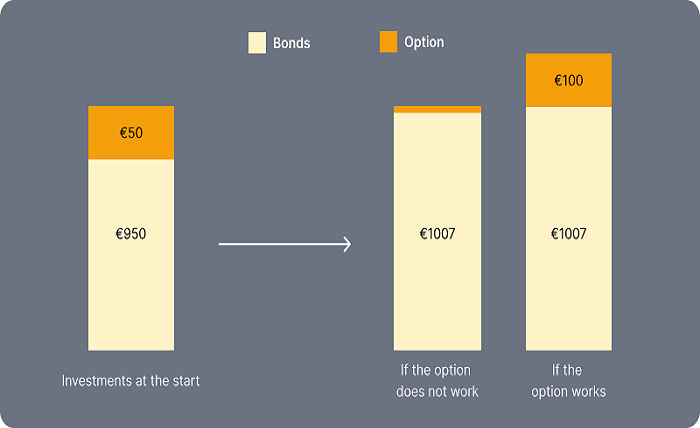

Think of them as financial Frankenstein’s monsters—but in a good way. Banks take a regular bond (the safe part) and stitch on a derivative (the growth part). The bond portion tries to protect your principal, while the derivative gives you returns linked to something like Nifty 50 or a basket of stocks. When these products are “listed” on NSE or BSE, they become eligible for special tax treatment that can save you serious money.

The 12-Month Rule: Your Tax-Saving Superpower

Here’s the simple math that changes everything:

- Sell before 12 months: Your profit is taxed at your income tax slab (could be 30%+)

- Sell after 12 months: Your profit is Long-Term Capital Gain, taxed at just 12.5%

Plus, you get a ₹1.25 lakh exemption every year on these long-term gains. So if your profit is ₹1.25 lakh or less, you pay zero tax.

But Wait—There’s Fine Print (Always)

Before you jump in, let me give you the real talk on risks:

- Complexity: These aren’t your plain-vanilla FDs. You need to understand exactly how returns are calculated. Some products have caps (“maximum 12% return even if Nifty goes up 30%”). Some have conditions (“you get returns only if Nifty stays above 18,000”). Read the terms like you’re reading your daughter’s wedding contract.

- Credit Risk: Your money is only as safe as the bank that issued the product. If the bank goes under, your “capital protection” means nothing. Stick to top-tier banks and financial institutions. That extra 1% return from a shady issuer isn’t worth the sleepless nights.

- Liquidity: Just because it’s “listed” doesn’t mean it’s easy to sell. The secondary market for these products can be thin. If you need money urgently before maturity, you might have to sell at a big discount. Only invest money you can lock away until maturity.

- The Tax Twist: Remember, the 12-month rule applies to the capital gains portion. If the product pays periodic interest (some do), that interest is taxed as regular income in the year you receive it. Don’t assume your entire return gets the sweet LTCG treatment.

How Anand Rathi Helps You Navigate This Minefield?

Look, I’m not going to pretend you should figure this out alone. Products this complex need expert guidance. Anand Rathi shares and stock brokers has a dedicated team that actually understands these instruments (not just sells them). They break down the payoff structure in simple language, explain the credit risk of different issuers, and help you plan your investment horizon to hit that 12-month sweet spot.

What I appreciate is they don’t push the highest-commission product. They ask about your goals first. Need principal protection? They’ll show you conservative options. Want higher returns and can take some risk? They’ll explain equity-linked notes with clear risk warnings. For clients with PMS investment, they integrate structured products as a satellite allocation—maybe 10-15% of the portfolio—to add stability and tax efficiency.

Bottom Line: Time It Right, Win Big

Listed structured products aren’t for everyone. But if you have ₹5-10 lakhs you can park for 12+ months, and you’re tired of FDs that don’t beat inflation, they deserve a look. It’s important to plan your getaway from the beginning. Write down the date of the month that starts the next year. Write it down. Tell your CA. Because that one month is the difference between giving away 30% of your profit versus keeping most of it.

Don’t be like Rajesh, celebrating too early. Be the smart investor who knows that in finance, timing isn’t just about buying and selling—it’s about waiting just long enough to let the tax laws work in your favor.